Introduction

Imagine trying to explain how the internet works to someone in 1995. You would probably mention websites, emails, and connecting cables, but it would still sound like science fiction. Today, we face a similar challenge with a groundbreaking innovation: blockchain. If you have spent any time online recently, you have likely run into this buzzword. It is frequently mentioned alongside Bitcoin, digital art, and the future of global finance. However, for most people, the concept remains wrapped in complex technical jargon that makes it hard to grasp.

This beginner confusion around blockchain is completely normal because the technology flips our traditional understanding of data and trust upside down. Most of our digital world relies on a central authority, such as a bank, a social media company, or a government database, to keep track of information. Blockchain changes this rule by sharing that responsibility among thousands of computers simultaneously. It can help beginners understand blockchain more easily if we strip away the confusing code and look at the core ideas instead.

In this comprehensive guide, you will learn exactly what this system is, how it functions behind the scenes, and why it is transforming industries far beyond digital currencies. We will break down complex concepts into everyday analogies, explore the different types of networks, weigh the benefits against the risks, and look at real-world applications. By the time you finish reading, you will possess a solid foundation in blockchain for beginners and be ready to navigate the decentralized future with confidence.

What Is Blockchain Technology?

To build a strong foundation, let us start with the most basic question: what is blockchain? In the simplest terms possible, a blockchain is a shared, digital ledger that records information in a way that makes it incredibly difficult to change, hack, or cheat the system. Think of it as a digital notebook that is copied and distributed across a massive network of computers worldwide. Every time a new transaction occurs, a record of that transaction is added to every single participant’s notebook in real-time.

This system is often referred to as distributed ledger technology (DLT). In traditional databases, a central administrator controls the data. For example, your bank maintains a private ledger of your account balance. If the bank’s database goes offline or gets hacked, your data is compromised. Moreover, you must trust that the bank is keeping accurate records. A distributed ledger removes this single point of control. Instead of trusting a centralized institution, the network relies on mathematics, cryptography, and community consensus to verify information.

When we look at blockchain , it helps to picture a shared Google Doc rather than a locked Word document. When you create a Word document, you lock it and send it to someone else, waiting for them to make changes and send it back. A Google Doc, however, allows multiple people to view and edit the document at the exact same time. While a blockchain is much more secure and restrictive than a Google Doc, the core idea is similar: everyone in the network has access to the exact same version of the truth simultaneously. This structural shift forms the basis of all crypto blockchain basics.

How Blockchain Works

Understanding the mechanics of this technology does not require a computer science degree. The name itself gives away the secret of its structure: it is literally a chain of individual blocks. Each block contains a specific piece of data, such as a financial transaction, a medical record, or a shipping update. Once a block is filled with information, it is securely locked and chained to the previous block using advanced mathematics. This continuous sequence creates an unchangeable timeline of data.

Three fundamental pillars keep this system operating smoothly and securely:

- Decentralization: No single entity controls the network. Power and information are distributed equally among thousands of independent computers called nodes.

- Immutability: Once data is written into a block and added to the chain, it cannot be altered or deleted. To change a single record, a hacker would have to alter that record on more than half of the computers in the network simultaneously, which is practically impossible.

- Transparency: Anyone can view the transaction history of a public blockchain. While your real identity is protected behind digital numbers and letters, the movement of assets is fully visible to the public.

To keep all these independent computers on the same page, the network uses a validation method known as a consensus mechanism. Because there is no boss or central server to declare which transactions are real, the computers must follow a strict set of built-in mathematical rules to agree on the current state of the ledger. Once the majority of the computers agree that a batch of transactions is legitimate, the new block is officially added to the chain, and everyone updates their personal copies of the ledger.

Key Blockchain Terms Table

| Term | Simple Meaning | Why It Matters |

| Blockchain | A distributed ledger of transactions shared across a network. | It is the central concept for understanding decentralized systems. |

| Block | A digital bucket or collection of data and transactions. | It stores information securely and links to other blocks. |

| Node | An individual computer connected to the blockchain network. | It maintains, shares, and validates the entire history of the ledger. |

| Consensus Mechanism | A built-in protocol or method used by nodes to agree on data. | It ensures trust, fairness, and security without a central leader. |

| Hash | A unique digital fingerprint generated for each individual block. | It maintains data integrity by changing completely if data is altered. |

| Smart Contract | Self-executing code stored on the network that runs automatically. | It eliminates middlemen and enables decentralized applications. |

| DApp | A decentralized application built on top of a blockchain. | It shows the practical use of blockchain beyond simple currency. |

Types of Blockchain Networks

Not all blockchains are built the same way. Depending on the platform and use case, a network can be designed to be completely open to the public or highly restricted for private enterprise use. There are four primary types of blockchain networks used today:

- Public Blockchains: These networks are completely open and permissionless. Anyone with an internet connection can join, view transactions, and participate in the consensus process. Bitcoin and Ethereum are primary examples. They offer maximum decentralization but can suffer from slower speeds.

- Private Blockchains: These networks operate on a permissioned basis, meaning a single organization controls who is allowed to enter, view, or modify the data. They are highly efficient and fast, making them popular for internal corporate testing, though they sacrifice true decentralization.

- Consortium Blockchains: Also known as federated blockchains, these networks are managed by a group of multiple organizations rather than a single entity. For example, four major banks might cooperate to run a shared ledger. This balances security with collaborative control.

- Hybrid Blockchains: This structure combines elements of both public and private systems. An organization can run a private network for sensitive internal data but connect it to a public chain to verify specific transactions or certificates publicly without exposing private details.

Major Benefits of Blockchain

The global excitement surrounding distributed ledger technology exists because it solves a fundamental human problem: how to establish trust between strangers online without relying on an expensive middleman. Here are the core benefits this technology brings to the digital landscape:

- Enhanced Security: Data is verified through cryptography and spread across a vast web of computers. This architecture eliminates single points of failure, making the network incredibly resilient against traditional cyberattacks and server outages.

- Unmatched Transparency: Because every node keeps an identical copy of the ledger, tracking the history of an asset is simple. Anyone can audit the public records, which builds deep accountability in financial and logistical systems.

- Removal of Intermediaries: Traditional systems require brokers, clearinghouses, and banks to validate transactions. Blockchain automates this verification process through code, which can drastically cut down transaction fees and processing times.

- Increased Efficiency: Instead of maintaining separate, siloed databases that require constant manual reconciliation, organizations can use a single shared ledger. This streamlines record-keeping and reduces administrative friction.

- Fraud Prevention: Because blocks are permanently time-stamped and chronologically linked, it is virtually impossible to fabricate historical data, file double payments, or forge digital ownership certificates.

Limitations and Security Risks

While the advantages are impressive, it is vital to remember that blockchain benefits and risks go hand in hand. No technology is perfect, and implementations depend heavily on platform design and technical execution. Beginners should study the basics carefully and look at the limitations before using blockchain services or investing in crypto assets.

- Scalability Issues: Public blockchains can be notoriously slow. Because every transaction must be verified by multiple nodes across a global network, processing speeds often lag behind traditional centralized payment processors like Visa.

- High Energy Consumption: Specific consensus mechanisms, like the Proof of Work system used by Bitcoin, require computers to solve complex math puzzles. This process demands a significant amount of electricity, raising environmental concerns.

- Regulatory Uncertainty: Governments around the world are still figuring out how to handle decentralized networks and digital assets. Sudden shifts in laws, tax rules, or compliance standards can drastically impact the survival of blockchain projects.

- Technical Complexity: Managing digital keys, interacting with decentralized applications, and understanding blockchain mechanics involves a steep learning curve. Simple user mistakes, like losing a private wallet password, can lead to permanent loss of assets.

- Implementation and Smart Contract Flaws: While the underlying blockchain network might be perfectly secure, the custom smart contracts written by human developers can contain coding bugs. Hackers often exploit these software vulnerabilities to drain digital funds.

Real-World Blockchain Applications

Although this technology started as the backbone for digital cash, its unique properties have sparked a wave of creative blockchain applications across dozens of traditional industries. Here is how decentralized ledgers are changing the real world today:

- Cryptocurrency: This remains the most famous application. Digital currencies like Bitcoin allow individuals to store and transfer wealth globally without needing a bank account or a central government.

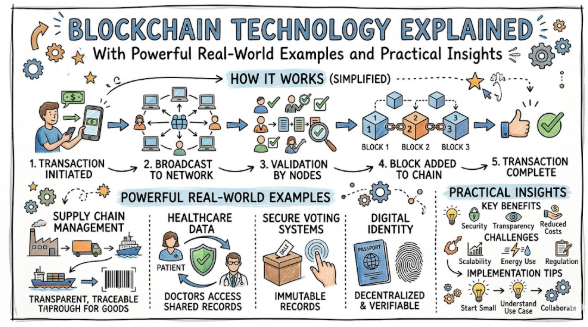

- Supply Chain Management: Companies can use a ledger to track a product’s journey from raw materials to the retail shelf. For instance, a grocery store can track the exact farm where a head of lettuce was grown, making it easy to trace contamination issues within seconds.

- Healthcare Systems: Patient privacy and data sharing are major hurdles in medicine. Blockchain can securely store medical records, allowing different hospitals to access a patient’s history instantly with their explicit cryptographic permission.

- Decentralized Finance (DeFi): This sector replaces traditional financial services like lending, borrowing, and trading with automated smart contracts. Users can access financial tools directly from their wallets without credit checks or bank managers.

- Digital Identity and Voting: Governments can create unforgeable digital IDs to prevent identity theft. Similarly, voting systems built on a ledger can guarantee that votes are counted accurately and cannot be altered after the fact.

- Non-Fungible Tokens (NFTs): These digital certificates prove absolute ownership of unique digital items, such as artwork, music, collectibles, or in-game items, opening up new economies for digital creators.

Step-by-Step Explanation of a Blockchain Transaction

To see how all these moving pieces fit together, let us walk through the lifecycle of a standard blockchain transaction. The entire process occurs in a matter of minutes, or even seconds, depending on the network being used.

The Transaction Flow

- Initiating the Transaction: A user decides to send an asset, like a digital coin, to a friend. They open their crypto wallet, paste their friend’s public address, enter the amount, and hit send.

- Broadcasting to the Network: The wallet signs the transaction with the user’s secret private key for security. The transaction details are then broadcast out to the decentralized peer-to-peer network of nodes.

- Entering the Pending Pool: The transaction enters a temporary waiting room filled with other unverified transactions from users around the world.

- Validation by the Nodes: Individual computers in the network pick up these pending transactions and verify that the sender actually possesses enough funds and that the digital signature is valid.

- Bundling Into a Block: Once verified, a group of these transactions is bundled together into a brand-new digital block by specialized nodes.

- Reaching Consensus: The nodes run the network’s consensus rules to ensure the new block is valid. Once the network reaches an agreement, the block receives a permanent time-stamp and a unique hash identifier.

- Adding to the Chain: The new block is permanently added to the existing blockchain. Every computer on the network updates its local ledger copy to reflect the change.

- Completion: The asset arrives safely in the friend’s digital wallet, and the transaction is complete, visible, and unchangeable.

A Simple Real-Life Example

Let us ground this process in a simple, non-technical scenario. Imagine a small town with four friends named Alice, Bob, Charlie, and Dave. They frequently borrow money from one another, but they are tired of carrying cash or worrying about who owes what.

Instead of opening a shared bank account, they decide to keep a shared notebook. Each friend keeps an exact copy of this notebook on their living room table.

One afternoon, Alice wants to send $10 to Bob. She calls a quick town meeting and shouts, “Hey everyone, I am transferring ten dollars from my account to Bob’s account. Please check your notebooks to make sure I actually have ten dollars!”

Charlie and Dave open their copies of the notebook, scan Alice’s past transactions, and see that she indeed has fifteen dollars left. They nod their heads and say, “Yep, the math checks out!”

At that exact moment, Alice, Bob, Charlie, and Dave all take out their pens and write down: Alice sends $10 to Bob at the bottom of their current page. Because everyone updated their notebooks at the exact same time, no one can lie later and claim the transaction never happened. If Dave tries to secretly erase the line in his notebook to save Alice some money, the other three friends will look at their own identical copies, see that Dave’s book does not match, and reject his altered version completely. This is the simple essence of a decentralized blockchain network.

Blockchain Technology Beginner Checklist

| Milestone Category | Learning Objective | Status |

| Foundational Concept | Can you explain the basic idea of a decentralized ledger to a friend without using jargon? | Yes |

| Core Architecture | Do you understand the literal difference between a digital “block” and the cryptographic “chain”? | |

| Vocabulary Mastery | Are you confident defining key terms like node, hash, smart contract, and DApp? | |

| Network Ecosystems | Can you identify the main structural differences between a public and a private blockchain? | |

| Trust Mechanisms | Do you grasp the basic role that a consensus mechanism plays in keeping independent computers in agreement? | |

| System Strengths | Can you list at least three distinct security and transparency benefits of using a blockchain? | |

| System Vulnerabilities | Are you fully aware of major industry limitations like scaling issues, energy costs, and smart contract bugs? | |

| Practical Utility | Can you name at least three real-world use cases for this technology completely outside of cryptocurrency? | |

| Transaction Dynamics | Do you understand the step-by-step flow of how an asset moves from a sender’s wallet to a receiver’s wallet? | |

| Risk Awareness | Do you acknowledge that actual safety, speed, and decentralization depend entirely on the specific platform and its implementation? | |

Common Beginner Mistakes to Avoid

When diving into a highly technical topic, it is incredibly easy to pick up misconceptions along the way. To keep your learning journey on the right track, be sure to avoid these common beginner traps:

- Confusing Blockchain with Cryptocurrency: This is the most common mistake. Blockchain is the foundational operating system, while cryptocurrency is simply the software running on top of it. Think of blockchain as the internet and Bitcoin as email.

- Believing Blockchain is 100% Risk-Free: Many people assume that because a blockchain is structurally secure, everything associated with it is immune to theft. Remember, while the underlying ledger is incredibly hard to alter, the platforms, websites, apps, and human inputs around it can still face security exploits.

- Ignoring Personal Security Basics: Beginners often leave their digital assets on unsecured platforms or lose their wallet recovery phrases. In a decentralized world, there is no “Forgot Password” button; keeping your private keys safe is entirely your responsibility.

- Misunderstanding Absolute Decentralization: It is easy to assume every project claiming to use blockchain is fully decentralized. In reality, many modern platforms sacrifice decentralization for faster speeds or corporate control, making them function more like traditional private databases.

- Following Media Hype Blindly: It is easy to get swept up in sensational news headlines or social media trends promising instant success. Always rely on thorough, objective research rather than hype before interacting with any blockchain application.

Practical Tips for Crypto and Tech Newbies

Stepping into the blockchain ecosystem can feel overwhelming at first. However, if you take a methodical, slow approach, you can build a deep understanding without exposing yourself to unnecessary risks.

- Learn Gradually and Patiently: Do not try to learn everything in a single weekend. Start by mastering the core concepts of data storage and decentralization before moving on to complex topics like cryptography or smart contract development.

- Utilize Test Networks for Practice: If you want to see how DApps and wallets function, use “testnets.” These are clone networks set up by developers that let you practice sending transactions using play tokens that carry zero real-world value.

- Always Use Secure Wallets and Platforms: If you decide to store digital assets or use decentralized services, stick to well-known, peer-reviewed hardware or software wallets. Enable multi-factor authentication and never share your seed phrase with anyone.

- Cross-Reference Your Research Material: The blockchain space moves incredibly fast. When reading guides or tutorials, verify the information across multiple reputable industry sources to ensure the technical details are accurate and up to date.

- Understand Platform Dependencies: Always remember that a blockchain’s performance, safety, and decentralization levels depend entirely on its specific platform and use case. Treat every individual blockchain project as its own distinct ecosystem.

When to Explore Blockchain Applications

You might be wondering if it is time to take your knowledge a step further and interact with real decentralized systems. Exploring practical blockchain applications makes a lot of sense during the following milestones:

- Conducting Investment Research: If you are planning to diversify your financial portfolio into digital currencies or tech stocks, studying the underlying blockchain architecture is essential for assessing long-term viability.

- Improving Supply Chain Visibility: If you run a business involving complex manufacturing, shipping, or logistics, exploring enterprise blockchain solutions can help you streamline inventory tracking and build trust with clients.

- Pursuing a Modern Tech Career: The demand for blockchain-literate developers, project managers, and consultants is growing rapidly. Learning the mechanics of distributed ledgers can give your professional resume a massive edge.

- Building Decentralized Applications: If you are a software engineer or hobbyist programmer, learning how to write smart contracts on platforms like Ethereum opens up a whole new world of app development possibilities.

Frequently Asked Questions (FAQ)

Q1: Can data on a blockchain ever be deleted or edited?

A1: Generally, no. Once a block is verified and added to the chain, its contents become permanent due to cryptographic links. Altering historical data requires controlling more than half of the network’s computing power, which is practically impossible for mature public networks.

Q2: Is blockchain technology the same thing as Bitcoin?

A2: No, they are entirely different. Blockchain is the underlying database technology that records transactions securely. Bitcoin is simply the very first cryptocurrency that was built using blockchain technology to function as digital money.

Q3: Who invented blockchain technology?

A3: The blueprint for blockchain was introduced in 2008 by an anonymous programmer or group of programmers using the pseudonym Satoshi Nakamoto. They created the system specifically to serve as the ledger for the Bitcoin network.

Q4: Do I need a powerful computer to use a blockchain?

A4: No, you do not. Running a validator node can require substantial computing power, but simply using a blockchain to send transactions, check records, or interact with applications only requires a standard smartphone or laptop with an internet connection.

Q5: What makes a blockchain so secure against hackers?

A5: Security comes from decentralization and cryptography. Instead of attacking one central server, a hacker would need to compromise thousands of independent computers simultaneously. Additionally, each block is locked with a unique cryptographic fingerprint that breaks if data is tampered with.

Q6: What are the main disadvantages of using blockchain?

A6: The primary hurdles include slower transaction processing speeds compared to central databases, high energy consumption for certain networks, complex interfaces for beginners, and a lack of clear, unified global regulations.

Q7: What is a smart contract in simple terms?

A7: A smart contract is a digital agreement stored on a blockchain that executes automatically when specific conditions are met. It acts like a digital vending machine: you drop in a token, the code verifies it, and it instantly delivers the item without needing an employee.

Q8: Are private blockchains genuinely decentralized?

A8: No, they are not. Private blockchains are controlled by a single organization or a select group of approved users. While they use blockchain’s secure, cryptographic block structure to store data, they lack the open, public decentralization found in networks like Bitcoin.

Q9: How long does a typical blockchain transaction take to finish?

A9: Processing times vary wildly based on the network and traffic levels. Some older networks can take anywhere from ten minutes to an hour to fully confirm a transaction, while newer, highly optimized platforms can settle transactions in just a few seconds.

Q10: Can a business use blockchain without using cryptocurrency?

A10: Yes, absolutely. Many enterprises use private or consortium blockchains strictly to track logistics, store corporate records, or verify medical data. These internal business setups do not require digital tokens or financial cryptocurrencies to function.

Conclusion

Understanding the world of distributed ledgers does not have to be an exhausting process. When you look at blockchain technology explained in simple language, you can see that it is ultimately just a secure, shared digital notebook that allows people to trust one another and transact directly without expensive middlemen. While it has completely revolutionized the world of global finance through cryptocurrencies, its true power lies in its ability to bring transparency, immutability, and security to almost every major industry on earth.

As you continue your educational path, remember to approach this ecosystem with an open mind and a healthy dose of responsibility. Blockchain concepts, application performance, and overall security features depend heavily on technology and implementation choices. It is highly recommended that you take your time, practice using secure wallets and platforms, and fully study the basics before investing your time or hard-earned money into any digital asset.